The Effect of Student Loan Debt on Homeownership

Writers and politicians are very concerned about increasing costs of college and student loans on the average young person. The amount of outstanding student debt in the US is now $1.25 trillion, and debt is a prerequisite in getting a degree and joining the labor force. This has coincided with a decline in homeownership in the US to a period we aven’t seen in the 60s, with similar low rates for young buyers. As home prices are higher in California, expenses that hurt young people’s ability to save translate into more drastic effects on Millennial homeownership in California.

A recent C.A.R. poll showed that almost 60% of California Millennials said that they were very concerned about their overall debt; further student loans were rated as the most worrisome type of debt. In the U.S. as a whole, student loans have replaced credit cards as the second most amount of debt held (behind mortgage debt).

Do higher levels of loan debts affect homeownership? As it turns out, having a college degree is a much bigger determinant of homeownership than the amount or existence of student debt and that the weak labor market since the Great Recession has affected homeownership more than debt. Between the recession and now, the rate of homeownership dropped from 35% to 26% for degree holding millennials, and from 23% to 17% for non-degree holding millennials.

There is ample evidence that student loans hinder the ability to accumulate wealth and thus delays homeownership. But over the long term this evens out. People who have successfully completed college degrees have higher earnings over their lifetimes than those without. While non-degree seekers own more homes than degree seekers in their early 20s, by the time they turn 27, that reverses. By the age of 30, people who graduated with student debt have the same homeownership rates as people who graduated debt free.

The amount student loan debt is much less than what is often written about in the media. The typical borrower has an average debt of $25k, with a median of $13k. Thirteen percent of borrowers have more than $50k of debt, and 3% of borrowers have more than $100k (a majority of these borrowers have also gone to graduate school).

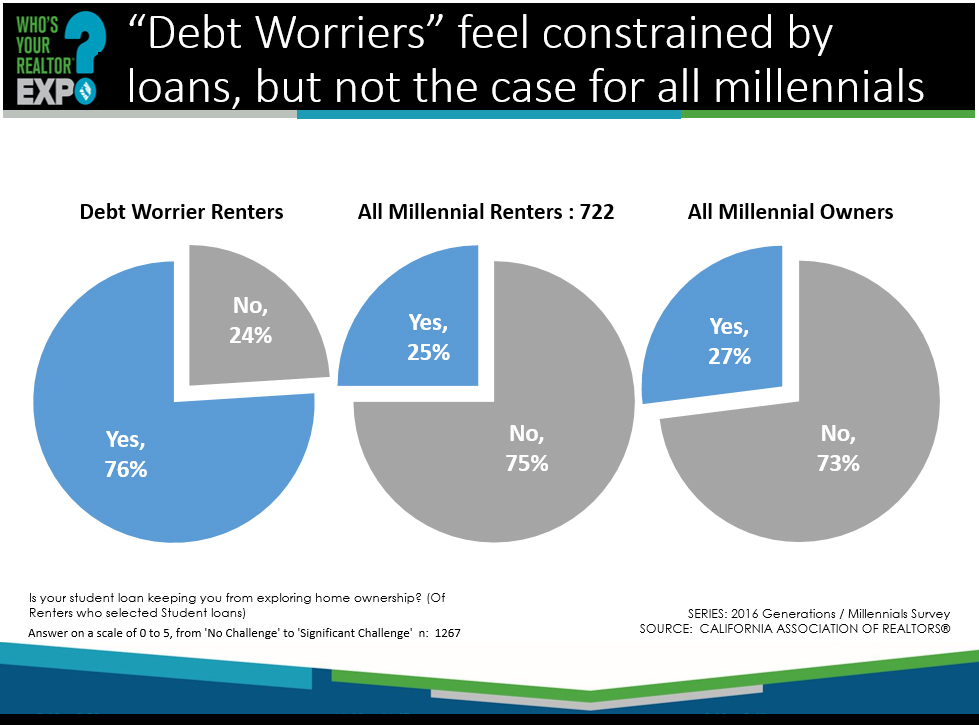

C.A.R. asked millennials who have purchased whether they thought that student loans were delaying their homeownership. Of millennials who were most worried about debt, 76% claimed that it kept them from homeownership; but only 25% of all millennials said that it was. When Millennial home purchasers were asked same question, 27% said that debt delayed purchasing. Homeownership and student loans are linked, but not in as drastic a way that many writers worry about.